Does a Rebuilt Title Affect Insurance?

Yes, a Rebuilt title affects insurance a great deal! In fact:

Rebuilt title insurance costs can be about 20-50% higher than a car with a clean title, and that is due to the perceived higher risk of rebuilt title cars.

Liability rates for rebuilt title insurance can often be the same as regular insurance, but collision/comprehensive may be cheaper since the vehicle’s value is lower.

Below, I will address some additional questions and concerns you might have about rebuilt title cars and insuring them

Key Facts:

- Salvage title cars must be repaired and issued a rebuilt title before becoming insurable

- Most insurers only offer liability coverage for rebuilt cars, not full coverage

- Expect to pay between 20% and 50% more compared to regular car insurance

- Leading insurers like State Farm and GEICO provide rebuilt title policies

- You’ll need to provide proof of repairs and mechanic inspections

- You can save money on rebuilt title insurance by lowering your liability coverage

Related Articles To Read:

- How To Turn a Rebuilt Title to a Clean Title

- Does a Salvage Title Void Recalls?

- Can you finance a salvage title car?

- How To Sell a Salvage Title Car

- Banks That Finance Salvage Titles

- Flood Damage Cars

Table of Contents

What is a Rebuilt Title?

When a car suffers extensive damage and is deemed a total loss by the insurance company, it will initially receive what is called a Salvage Title.

Salvage title cars cannot be legally driven or registered in ANY state, and this is where Rebuilt Titles come in.

Once a salvaged car is rebuilt to state roadworthiness standards, it receives a rebuilt title. Now, it can be registered, driven, and insured again, albeit often with limitations.

Here’s an overview on:

| Title Type | Repaired? | Insurable? | Drivable? |

|---|---|---|---|

| Salvage | No | No | No |

| Rebuilt | Yes | Yes* | Yes |

*Usually, liability-only policies

The key difference is that a rebuilt title proves past repairs, while a salvage title signifies an unfixed, undrivable total loss vehicle.

Which Companies Insure Rebuilt Title Vehicles?

Car insurance companies known to cover rebuilt title cars are:

| Insurance Company | Extent of Coverage for Rebuilt Titles | Rating |

|---|---|---|

| USAA | Liability, Comprehensive, Collision | 5/5 |

| American Family | Liability, may require photos for other coverages | 4/5 |

| Farmers | Liability, Comprehensive, Collision | 4/5 |

| Infinity | Liability | 3/5 |

| Kemper | Liability, Comprehensive, Collision | 3/5 |

| Nationwide | Liability only, unless damage was purely cosmetic | 4/5 |

| Root | Liability, Comprehensive, Collision | 4/5 |

| State Farm | Liability, Comprehensive, Collision | 5/5 |

| The General | Liability | 3/5 |

| 21st Century | Liability | 3/5 |

Start your search with these highly-rated insurers first when exploring rebuilt car coverage options. Be sure to ask about costs, inspection needs, exclusions, and document requirements before purchasing a policy.

Are Rebuilt Title Cars Harder To Insure?

Yes, as you would expect, it is more difficult to insure a vehicle with a rebuilt title, and the reason is simple…

Why Is a Rebuilt Title Harder to Insure?

Even after repairs, insurers view rebuilt title cars as riskier investments due to their history of extensive damage. As a result, policies often come with restrictions.

Restrictions & Limitations of Rebuilt Title Insurance

- Only liability coverage is available, not full coverage with collision/comprehensive

- Special mechanic inspections are required

- Lower payouts if the car is totaled again

- Premiums are 20%- 50% higher than regular insurance

The Pros and Cons of Rebuilt Title Insurance

Before moving forward with the purchase of a car with a rebuilt title, or any other branded title, you should weigh the pros and cons.

Yes, a rebuilt title car will be significantly cheaper, and you can also then afford to buy a much newer or larger vehicle with the savings. But the cost of insuring the car might end up canceling out that savings later…

| Pros | Cons |

|---|---|

| Lower purchase price compared to clean title vehicles | Lower resale value due to title status |

| Extensive repair documentation may be available | More difficult to get full insurance coverage |

| Damage may not be as severe as it seems | Potential for lingering issues from repairs to surface later |

| Opportunity for a good deal if thoroughly inspected | Most lenders won’t provide financing |

| Manufacturer’s warranty is typically voided | |

| Extensive inspection required to assess repair quality |

Steps to Get Insurance for a Rebuilt Title Car

Follow these key steps for securing coverage:

Repair Vehicle and Obtain Rebuilt Title

- To switch from a salvage to rebuilt title, repair damage through a licensed mechanic

- Submit proof of repairs and pass your state’s inspections

- Apply at the DMV for a rebuilt title

Shop for Insurance, Comparing Quotes

- Start with quotes from known rebuilt title insurers like State Farm

- Expect restrictions on comprehensive/collision with most companies

- Ask about any extra inspection requirements

Provide Documentation for Past Repairs

Common documents needed:

- Rebuilt title certificate

- Mechanic’s statement confirming roadworthy repairs

- Before/after photos of car

- Original repair estimate from rebuilder

- Receipts proving quality of restoration

With paperwork confirming repairs, insurers gain confidence in mitigated risks.

What Rebuilt Title Insurance Coverage Can I Get?

Liability insurance is widely available for rebuilt cars, covering injury or damage you cause others. However, adding coverage like collision or comprehensive is often limited or unavailable.

Collision covers your repair costs after an at-fault accident. Comprehensive handles non-crash damage like weather, theft, or animal incidents.

Due to reduced resale value, the potential payout an insurer would make for rebuilt title cars is lower compared to clean title vehicles, making them hesitant to provide extensive coverage.

Some insurers like State Farm and GEICO may offer full coverage policies on a case-by-case basis after inspections or proof of quality repairs. This involves providing documentation like repair invoices and mechanic statements. However, it’s best to anticipate only liability insurance availability to avoid surprises.

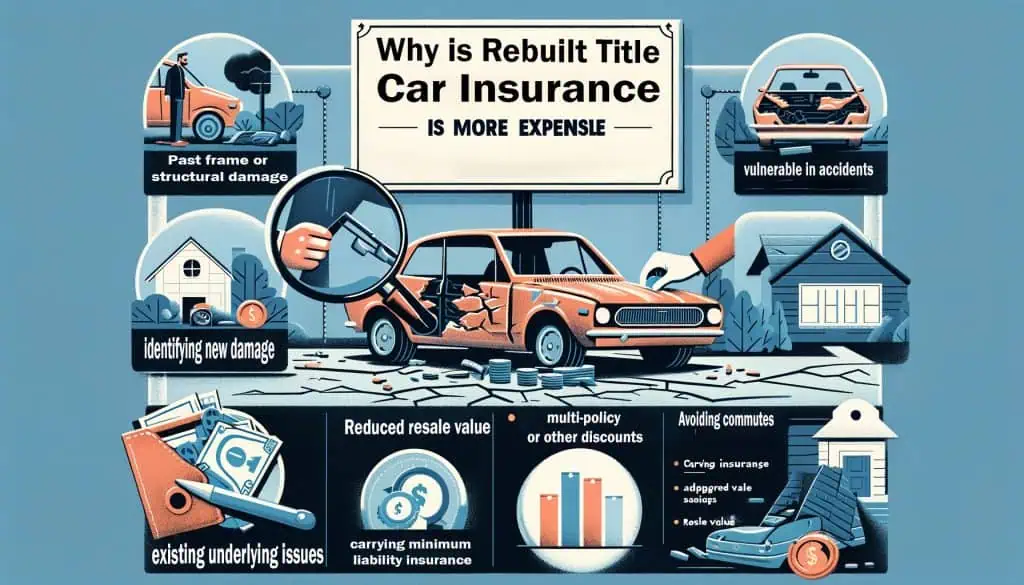

Why is Rebuilt Title Car Insurance More Expensive?

Insurers classify rebuilt title vehicles as higher-risk, leading to premiums up to 20% higher compared to clean title policies.

Statistical reasons include:

- Past frame or structural damage makes cars more vulnerable in accidents

- Difficulty identifying new damage versus existing underlying issues

- Reduced resale value increases potential loss ratio for insurer

- Assumption drivers couldn’t afford a newer clean title vehicle

Essentially insurers fear taking on cars likely to cost more money over time, whether from increased accident rates or pricier comprehensive claims.

How to Save Money on Rebuilt Title Insurance

Fortunately, there are several ways you can lower the cost you’ll have to pay to insure a rebuilt title vehicle:

- Shop around for multiple quotes

- Only carry the minimum liability insurance required in your state (Not recommended)

- Qualifying for multi-policy or other discounts

- Finding carriers competing for rebuilt car customers

- Maintain a good driving record and some companies will lower your rates over time

How to Get Insurance on Rebuilt Salvage Cars By State

When shopping for insurance coverage options on a car with a rebuilt title, certain state-specific requirements must first be satisfied. Rules, inspections, and documentation vary but typically follow a standard process across most regions. Here are some examples below:

South Carolina Rebuilt Title Car Insurance

- Repairs: Damaged vehicles cannot be insured in South Carolina until they receive rebuilt titles after sufficient repairs.

- Inspections: Cars with rebuilt titles must pass state safety inspections focused on roadworthiness.

- Paperwork: Proof of past repairs and documentation of current mechanical integrity is often required.

- Coverage: At a minimum, liability insurance is usually available, but comprehensive and collision insurance may still be difficult to obtain in some cases.

Florida Rebuilt Car Insurance Regulations

- Repairs: Like South Carolina, repairs solving past damage must be completed before rebuilt titles and insurance eligibility opens up.

- Inspections: Approved safety inspections are necessary in addition to mechanical repairs.

- Paperwork: Documents confirming repairs have been finished properly will need to be provided to potential insurers.

- Coverage: While liability coverage is commonly accessible with a rebuilt title, full coverage can still be limited for insurers in Florida.

California Rules for Insuring Rebuilt Salvage Vehicles

- Repairs: The salvage vehicle must be extensively repaired and brought up to minimum standards before earning a “revived salvage” title.

- Inspections: An official inspection, like one from the California Highway Patrol, must be passed to verify current roadworthiness.

- Paperwork: Key paperwork like proof of repairs, ownership, former title status, and inspection certificates must be provided.

- Coverage: At minimum liability insurance is available in some cases, but most insurers will restrict comprehensive and collision policies.

New York Rebuilt Title Insurance Requirements

- Repairs: To earn a rebuilt title eligible for insurance in New York, all prior damage must be repaired first.

- Inspections: Passing state DMV inspection processes focused on current mechanical integrity and drivability is mandatory.

- Paperwork: Insurers will require paperwork trail from repairs to inspection results before considering coverage.

- Coverage: Liability protection only may be widely available. But gaining any collision, comprehensive, or full coverage policies on rebuilt cars stays difficult in NY.

Key Takeaways for Rebuilt Title Car Insurance

In summary, follow these best practices:

- Repair past damage meticulously before applying for coverage

- Gather documentation proving repairs and roadworthiness

- Anticipate liability policies only, not full collision/comprehensive

- Compare quotes from specialty insurers comfortable with rebuilt risks

- Expect premiums potentially 20% higher than clean title cars

- Reduce policy costs through available discounts or minimal usage

Legal Disclaimer: The information provided in this article is for general informational purposes only and should not be considered legal, financial, or insurance advice. The risks and challenges associated with buying and insuring a rebuilt title car may vary depending on individual circumstances, state regulations, and insurance company policies. Always consult with a qualified legal professional, financial advisor, or licensed insurance agent before making any decisions regarding the purchase or insurance of a rebuilt title vehicle. The author and publisher of this article are not responsible for any actions taken based on the information provided herein, and readers assume full responsibility for their decisions and outcomes.

Sources and References For This Article:

- https://www.automoblog.net/research/insurance/how-to-get-auto-insurance-for-salvage-vehicles-and-rebuilt-titles/

- https://www.moneygeek.com/insurance/auto/how-to-get-car-insurance-salvage-title/

- https://www.marketwatch.com/guides/insurance-services/insuring-a-salvage-title-car/

- https://wallethub.com/answers/ci/salvage-title-south-carolina-1000037-2140749362/

- https://wallethub.com/answers/ci/salvage-title-florida-1000037-2140749226/

- https://freedomgeneral.com/blog/can-i-insure-a-salvage-title-in-california/

- https://wallethub.com/answers/ci/salvage-title-new-york-1000037-2140749338/

- https://wallethub.com/answers/ci/salvage-title-arizona-1000037-2140749213/